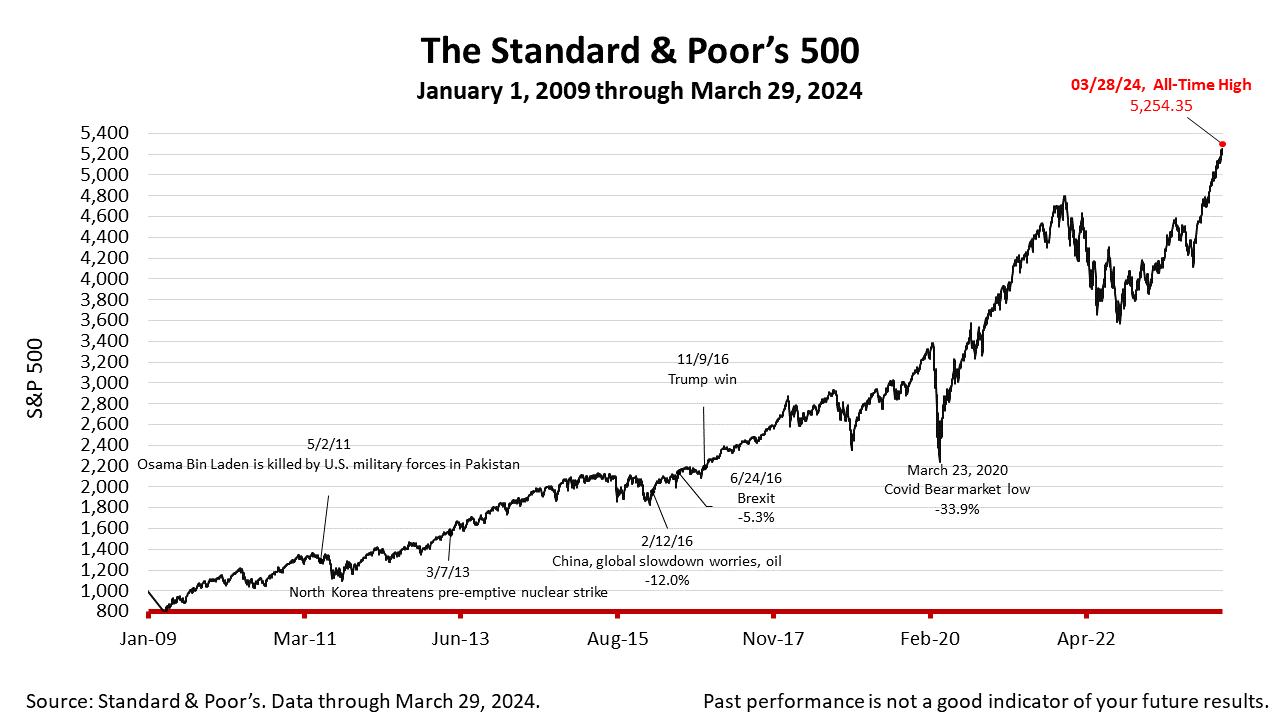

The Standard & Poor’s 500 stock index closed Friday at a new all–time high, ending the first quarter of the year with a gain of 10%. That’s as much as large-company stocks averaged annually since 1926. Amid widespread skepticism about the future, the U.S. financial economy is poised to continue to surprise retirement investors as well as Wall Street analysts.

The strong performance in the stock market, a measure of progress of the world’s leading democracy and largest economy, comes as investors expect the Federal Reserve to cut interest rates at the end of the second quarter and raise them once more late this year. Optimism is also fueled by the growing use of artificial intelligence, which is expected to boost productivity. The Standard & Poor’s 500 closed at 5254.35, up +0.11% from Thursday and +0.39% from a week ago. The index is up +134.84% from the March 23, 2020 Covid bear market low. The Standard & Poor's 500 (S&P 500) is an unmanaged group of securities considered to be representative of the stock market in general. It is a market-value weighted index with each stock's weight proportionate to its market value. Index returns do not include fees or expenses. Investing involves risk, including the loss of principal, and past performance is no guarantee of future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted. Nothing contained herein is to be considered a solicitation, research material, an investment recommendation, or advice of any kind, and it is subject to change without notice. Any investments or strategies referenced herein do not take into account the investment objectives, financial situation or particular needs of any specific person. Product suitability must be independently determined for each individual investor. Tax advice always depends on your particular personal situation and preferences. You should consult the appropriate financial professional regarding your specific circumstances.

The material represents an assessment of financial, economic and tax law at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Forward-looking statements are subject to certain risks and uncertainties. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources. It is not guaranteed as to accuracy, does not purport to be complete, and is not intended to be used as a primary basis for investment decisions.

This article was written by a professional financial journalist for Advisor Products and is not intended as legal or investment advice. |  Printer Friendly Version

Printer Friendly Version